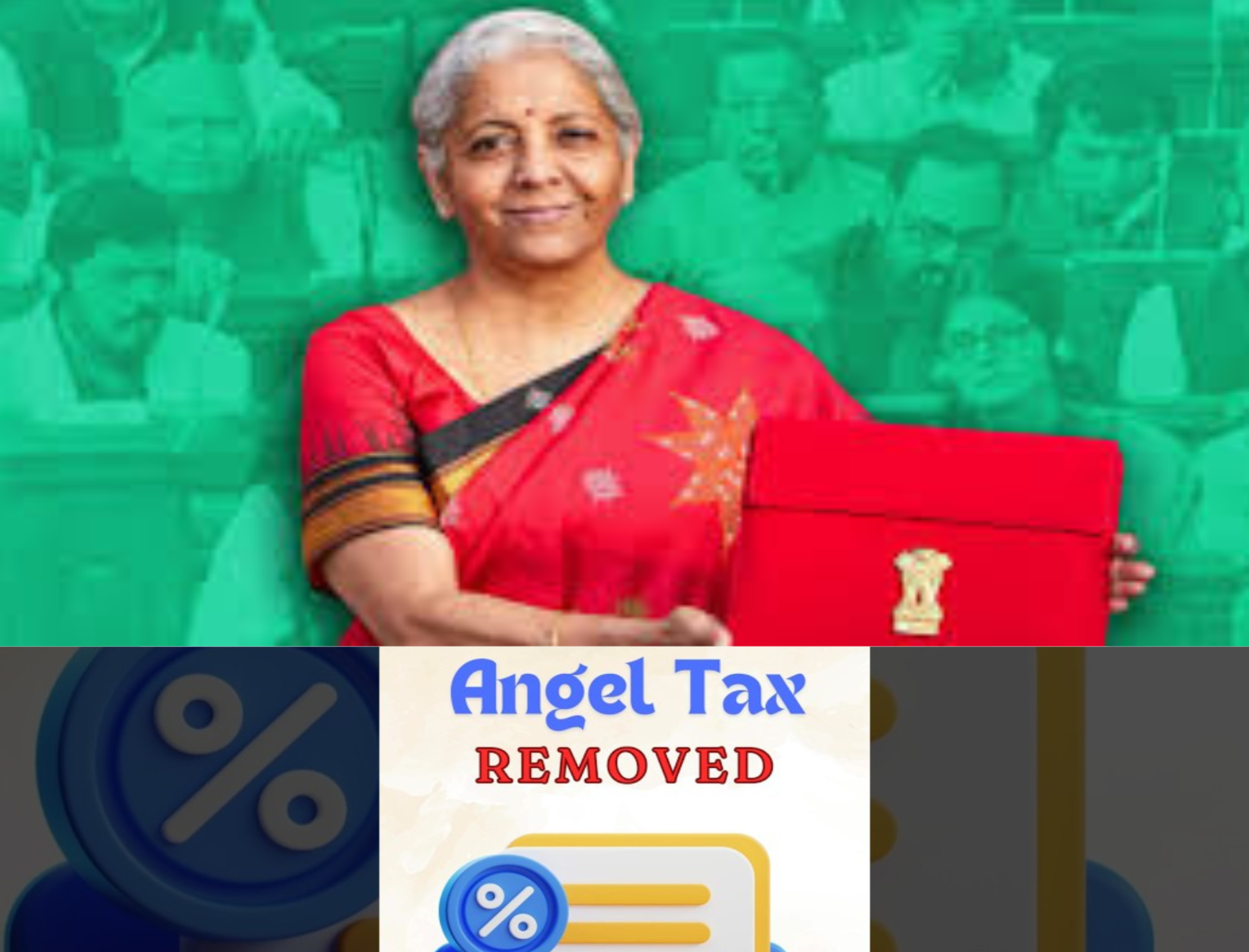

Breaking News

Angel tax scrapped

Union Budget 2024 brought a sigh of relief for startups and their investors as FM proposed to abolish Angel Tax of the Income tax Act 1961.

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley.

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley.

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley.

-

Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley.

What is Angel Tax?

- The idea of angel tax was first introduced in the Union Budget 2012 by then Finance Minister Pranab Mukherjee. The primary objective was to check money laundering practices through investments in startups and catch bogus firms after advent of such cases.

- Angel Tax, formally known as Section 56 (2) (vii b) of the Income Tax Act, is the tax imposed on funds raised by startups from angel investors which is only applicable to funds that exceed the fair market value of the company.

- For example, if a company's fair value is Rs 1 crore and it raises Rs 1.5 crore from angel investors, the excess amount of Rs 50 lakh is subject to this tax. Tax authorities considered the premium paid by investors as income, taxable at around 31 percent.

- Till 2023, this tax was imposed only on investments made by resident investors. However, it was extended to transactions involving foreign investors as well.

Startups aggravation on Angel Tax

- In recent years, many startups have expressed significant concerns regarding the angel tax, describing it as excessively unfriendly and unjust. They argued that determining the fair market value of a startup is impractical.

- Since its introduction, the interpretation of these provisions has been a topic of numerous debates among the corporates as various aspects remained unclear leading to controversies. This is further accelerated by Indian tax authorities rejecting the valuation methodology adopted by the taxpayer and adopting a contrary position while going beyond the intent of the legislation. A few issues include (a) failure of provisions to differentiate between legitimate investments and money laundering activities; (b) Tax officer rejecting the valuation methodology and undertaking fresh evaluation; (c) disparity with valuations prescribed under Foreign Direct Investment Regulations; (d) Valuation issues in case of issuance of shares by an Indian company in a distressed situation, right issues, bonus issues, amalgamation/demerger etc.; (e) applicability at the time of conversion of convertible instruments into equity, etc.

- Startups claim that Assessing Officers (AOs) often choose the discounted cash flow method to calculate this value, a method perceived to favour tax authorities over startups.

- Startups have categorically mentioned that they received tax notices on angel investment raised 3-4 years prior. In some instances, the total amount owed in taxes and late payment fees exceeded the original funding amount.

- At the height of the angel tax imbroglio in 2019, a survey by Local Circles showed that over 73% of startups that had raised capital between INR 50 lakh to INR 2 crore in India have received angel tax notice(s) from the Income Tax department.

- However, the 2019 Union budget, the government eased the angel tax rules by mandating that Department for Promotion of Industry and Internal Trade (DPIIT)-registered startups would be exempted from the provision. But the fine print showed that it was not a blanket exemption for all such startups. It applied only to those certified by a government body called the Inter-Ministerial Board (IMB).

- The IMB is a group of bureaucrats who certify whether a startup is innovative and worthy of receiving benefits under the Income Tax Act, 1961. Out of the 84,000 startups registered with the DPIIT as of now, less than 1 percent are IMB-certified.

A welcome move

- Reserve Bank of India (RBI) observed the sharp rise in consumer durable and other unsecured loans and instantly increased its risk weights. RBI governor Shaktikanta Das said in the recent monetary policy that the central bank was closely monitoring the rise in unsecured retail loans to determine if additional measures are necessary to moderate this lending. Concerned by the unbridled growth in personal loans, the RBI in November last year, increased the risk weights on unsecured loans. The move has resulted in higher capital requirements for banks and NBFCs, raising the cost of funds for borrowers.

- fication of the portfolio. Diversifying the portfolio will help reduce the portfolio risk and address the systemic risk that the regulator is concerned about from a financial stability standpoint. Having said that, the asset quality will still be a significant concern and the regulator expects the segment to make substantial investments in technology and governance to ensure that the quality of underwriting standards is not diluted and continues to remain robust.

Editor’s Note

The growing issue of unsecured loans in India has become a cause for concern. The RBI, noticing an increase in unsecured consumer loans such as personal and credit card loans, has made a significant decision. The RBI has decided to increase the risk weights for consumer lending, raising the buffer reserve to 25% for banks and NBFCs distributing consumer loans.

TRUEE NEWS BANGLA SHORT

BROADCAST CHANNELS